deven Ane hema>g 3 : 2 na p/ma`ma> nfo-nukxan vhe>cta Aek

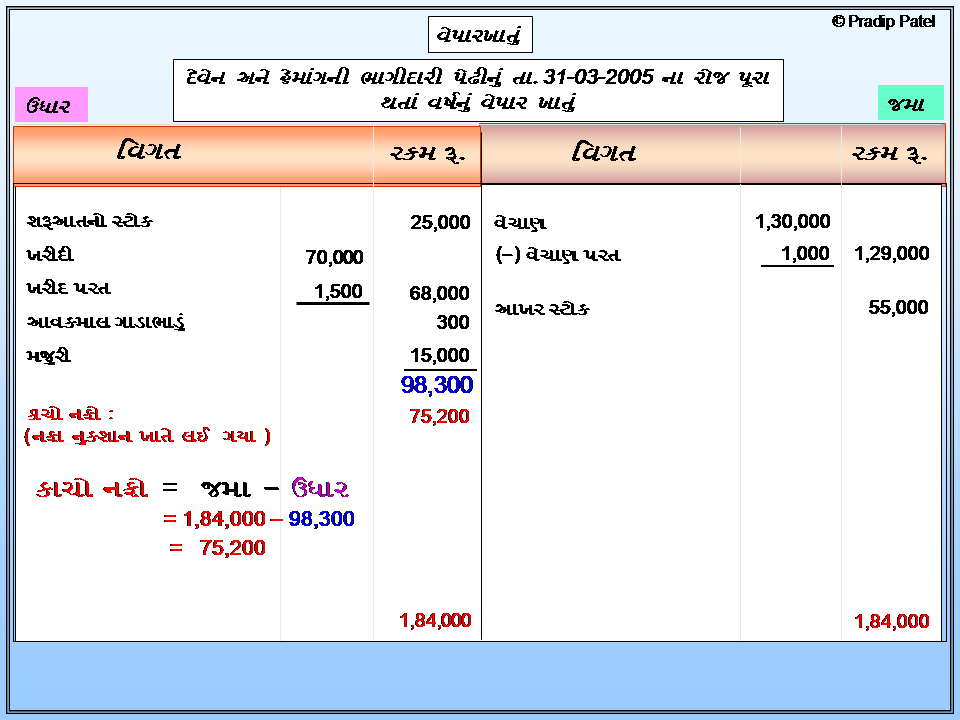

pe!Ina wagIdaro 0e. ta. 31-3-2005 na rojna nIce Aapela

kaca srvEya t4a hvala pr4I pe!Inavai8Rk ihsabo tEyar

kro.

hvalaAo :

(1) Aaqr S3ok ½.55,000 no 0e, jenI b=r ik>mt 10 % v2u 0e.

(2) wagIdarone mUDI pr vai8Rk 6 % Vyaj Aapvanu> 0e t4a

]paD pr Aa p/ma`e Vyaj vsul krvanu> 0e : deven ½. 400,

hema>g ½. 350

]paD pr Aa p/ma`e Vyaj vsul krvanu> 0e : deven ½. 400,

hema>g ½. 350

(3) y>Žt/o pr 10 % Ane finRcr pr 5 % leqe 2saro g`o.

(4) devadaro pr 5 % leqe xkm>d le`anI =egva{ kro.

(5) cUkvvana bakI qcaR : pgar ½. 400 ,prcUr` qcaR ½. 75, waDu ½.150.

it requires gujarati fonts

|

| Devan and Hemang Accounts Example for std 12 |

|

| Devan and Hemang Accounts Example for std 12 |

|

| Devan and Hemang Accounts Example for std 12 |

|

| Devan and Hemang sales Accounts Example for std 12 |

|

| Devan and Hemang profit and loss Accounts Example for std 12 |

|

| Devan and Hemang Profit & Loss Accounts Example for std 12 |

|

| Devan and Hemang Partner's Account Accounts Example for std 12 |

|

| Devan and Hemang Paku Sarvaiyu Accounts Example for std 12 |